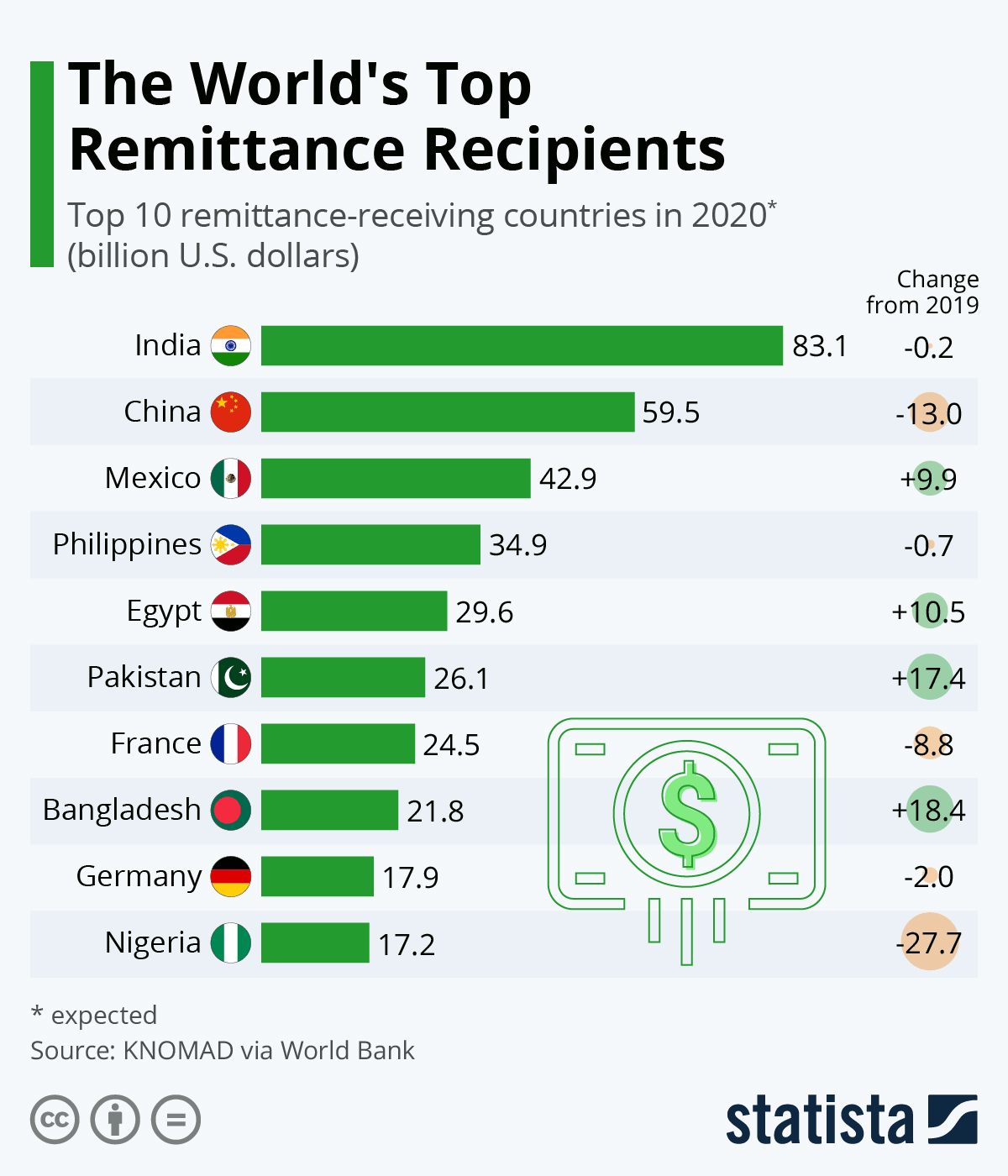

One of the most profitable use-cases of Bitcoin is the overseas remittance business. Remittance flows remained resilient over the last few years, with growth projected to continue at rates similar to those seen over the medium term. It has a value of more than $700 billion every year, and a major share of the money goes to low-middle-income countries.

With the rise in the remittance industry, we may expect it to reflect in the local economy as the purchasing power of citizens increases. But that is not the case in countries such as Nigeria, India, Vietnam, and Bangladesh.

The cost of transfer is so high in many of these countries that recipients have to pay at least 6% for smaller remittances, and it can go all the way up to 22%. South African Countries like Botswana also suffer from such high average fees.

Money transfer services are expensive due to complying with regulations in different countries and different exchange values. Additionally, there may be a lack of transparency in the exchange rates, adding another invisible cost to the consumer.

By having institutions and big banks run the remittance market in such a traditional way, countries that depend on overseas money inflow will suffer. In many of the African countries, remittance inflows account for a third of the entire GDP. So if they are charged with high cross-border transfer fees, it will limit their buying power, which will not help increase the demand.

Therefore, we need to start using a payment system that pairs cryptocurrencies like Bitcoin and reduce peer-to-peer transfer costs. When we have a network with zero intermediaries, it will automatically start benefiting recipients of remittances. To understand how drastic a difference it makes, let us take a step further and see how bitcoin transfers using the lightning network and Stripe application are disrupting global remittance markets.

Why are banks failing to provide direct remittance services?

While there are many money transfer companies, only a handful have direct access to the global correspondent banking network. Until the introduction of correspondent banking, cross-border payments involved higher risks of fraud and delay. Neither of the parties had a direct relationship, and there was no central authority responsible for clearing and settlement.

With CBRs in control of cross-border payments, the number of intermediaries increased, slowing down the transfer process and making it even more expensive. Most of these government institutions had no association with banks in third-world countries, so the power to regulate fees is concentrated in the hands of a few local banks of that particular state.

Over the last few years, we have seen 50% of CBRs get terminated, making foreign exchange services challenging and costly. African countries heavily relied on these banks for international trade, and now, they are asked to pay huge fees to receive their payments. That is why we see a shift in money transfers in terms of currency. Remittance flows in the form of USD reduced by more than 28%, so most citizens are now receiving money in the form of cryptocurrency.

Nigeria has the highest acceptance rate of bitcoin, and it is greatly helping with remittance flows. Banks cannot provide the same facilities, as they are excessively spending on KYC, Anti-money Laundering regulations, and other capital controls. With bitcoin’s network, it can become easier to manage P2P payment channels.

In developing countries, the financial system is usually unstable and cannot be relied upon, so banks have no other choice but to charge high fees for remittance payments. The solution here is- a micropayment channel that can serve as a payment solution for digital goods, where the costs are relatively low, and the transaction fee is negligible.

How can Blockchain make a difference in Remittance?

The cost of remittances is at the heart of the issue. The costs for sending money overseas can reach up to an astonishing 10% of the transaction if banks are involved and twice that if informal means are utilized by both migrant workers and family members back at home. Without a doubt, this is where blockchain technology can contribute to society by reducing costs considerably. There are three main opportunities for Blockchain to optimize remittance markets and overcome traditional banking challenging:

- Streamline the Remittance Process and Disintermediation

The remittance industry is a lot like the postal service, I mean, seriously… It’s physical mail. There are multiple steps and points of failure and hefty fees for the privilege of sending money. Multiple points of failure arise when only a few banks are operating exchange services at a large scale. As these intermediaries increase to meet the demand, they start to cut the transaction fee, increasing the amount the receiver ends up paying. Thanks to its efficient network of approving transactions, Blockchain technology can streamline a process that could otherwise take multiple days by removing intermediary parties.

- Mobile Wallets using Blockchain Tech

The main problem in emerging countries like Africa is mobile penetration. According to Statista, it is supposed to hit the 50% mark by 2025. When mobile penetration goes up, people will have easier access to applications like mobile wallets. With dozens of companies entering this space, we will see blockchain-powered wallets being an integral part of remittances. An example of a startup that utilizes cryptography mobile wallets in emerging markets is Coins.ph. With over 10 million Filipino users, they have opened the door to crypto for a new generation.

- Integration of Blockchain Solutions Within Current Traditional Players

The Blockchain is a disruptive technology, but it’s not designed to make competitors obsolete. Blockchain partners with banks and money transfer operators to give them a more streamlined way to send money worldwide. By strategically incorporating blockchain integration within their platforms, money transfer operators will take advantage of the increasingly popular crypto-currency landscape.

We have seen many new companies and startups trying to fill this gap in the remittance market, but very few have been successful. The strike is currently one of the few payment options, simplifying remittance flows and driving the cost of sending cross-border payments to zero. With the help of bitcoin’s lightning network, we see this fintech application make large strides in this industry. Let us see how it is disrupting remittance payments.

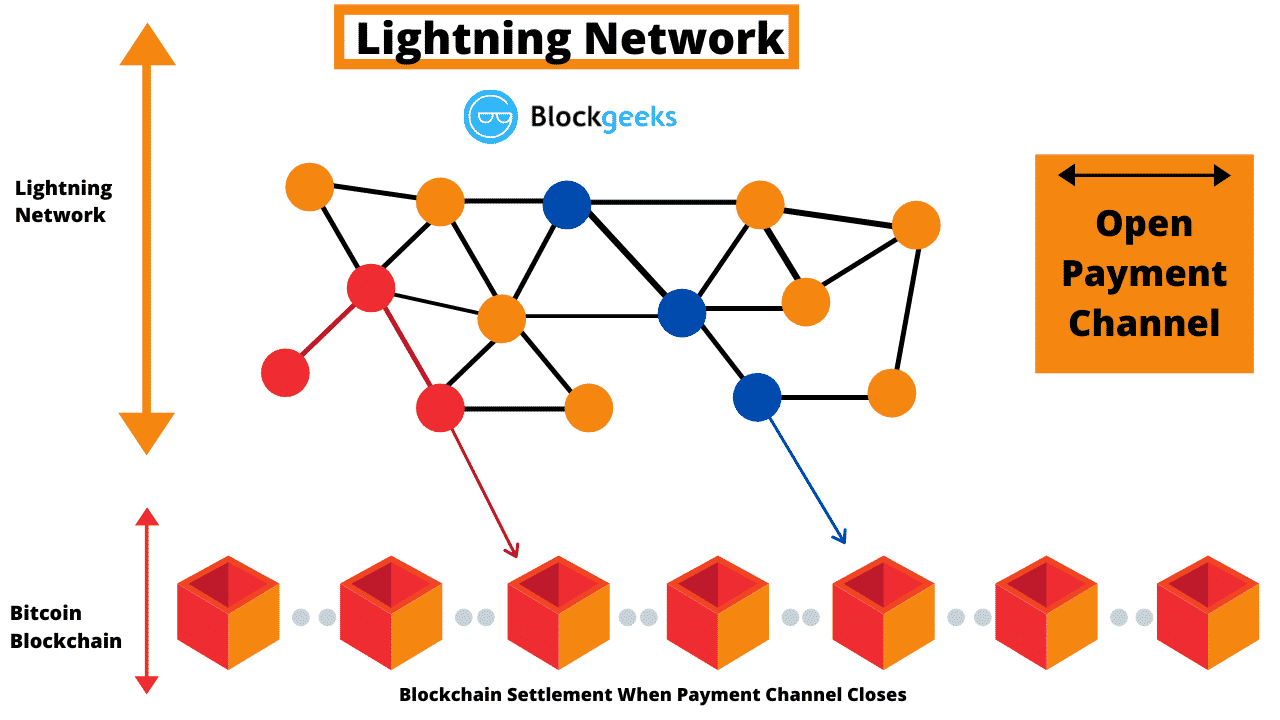

Bitcoin’s Lightning Network

The lightning network is innovated to solve bitcoin’s scalability issue. At its current rate, the bitcoin network can only process two to three transactions per second, which is not a reliable number for mass usage. With the help of the lightning network, we are seeing payment channels being created between two parties. It doesn’t matter how many transactions are performed in this payment channel. In the end, only one of them will be recorded on the bitcoin blockchain, which saves both time and money.

Structure

Bitcoin’s lightning network still needs to make improvements in speed and fees. The main difficulty for lightning networks is creating new channels and including more parties in one channel. If they can add new parties to the channel, it would reduce the load on the network, as we are combining existing payment channels. This will also improve the speed of off-chain transactions.

Lightning Network- Fee Mechanics

When making payments through the lightning network, users have to pay a minimal fee. The network categorizes this particular fee into two types: Base fee and fee-based on liquidity.

Base Fee

A flat rate is applied to all transactions that go through your node. You can charge 300 satoshis or 1 cent for routing payments. If the volume increases, you can decide to drop down the base fee. Node operators of the network set base fees based on their capital.

Liquidity Provider Fee

If you are an LP, you can set your fees based on how much liquidity a person is using, and it is charged for every Satoshi. Lightning Satoshi can charge you a fee for every Satoshi that is sent through your Lightning channel.

To make it even simpler, let us take the $10 payment done within the lightning network. It would take one Satoshi to complete the transaction, and it only takes 1 second. And the best part about using a lightning network is that it doesn’t cost higher fees when the volume increases. So if you are transferring more money back home, you are still charged in relative terms with a flat rate.

How is Strike impacting lightning networks?

Being a mobile application that uses bitcoin as an asset for transfer, Strike is helping users to maximize the potential of the lightning network. The best way to describe the platform is- a futuristic cryptocurrency platform that solves fiat money transfer and allows users to send money to anyone in the world instantly for a negligible cost.

The El Salvador case study will define how effective the lightning network is and how Strike is streamlining the whole process. The remittance services in El Salvador always relied on dollars from the US, but with lightning network, users can have the same inflows helping the GDP at a much lower cost in transaction fees.

Even though Strike does not have any revenue streams, Jack Mallers is confident in finding a successful business model once the merging of the lightning network proves sustainable. It’s safe to assume that Strike and other startups entering this space will disrupt the remittance industry, given the unique customer experience they aim to provide. When customers engage with brand-new payment options, they benefit from competitive and fast delivery processes and high-quality customer service.

Wrapping Up

International remittance is a multi-billion dollar industry, and the cost of transactions limits the amount that people can send. Bitcoin provides a faster way for people to transfer money to remote areas that need help due to higher transaction costs with typical remittance services. With lightning networks disrupting traditional methods, we can expect bitcoin the asset to be used to its full potential. Remittances are driving the economy in many countries, so it will be exciting to see how Stripe leverages the lightning network and attracts enough users to make it more sustainable.

Born and brought up in India, Karthikeya Gutta is a crypto journalist and freelance contributor for ItsBlockchain. He covers various aspects of the industry with in-depth analysis and research. His passion towards blockchain and crypto ecosystem is mainly because he believes it can really change the world and help millions of people.

Subscribe to get notified on latest posts.

{kind=link}