In our previous on-chain market analysis, we mainly discussed that bitcoin needs to reclaim the $53k level, which is the cost basis for short-term holders. Not only did we fail to reach that crucial level, but we saw a further drawdown to $41k. Previously, in December 2021, we saw a major build-up of open interest that caused extreme volatility to the downside.

Due to the FED news, the market reacted in ways we never expected. Many investors were aware that the Federal Reserve would raise interest rates. And that would reduce their holdings, and banks will limit bond purchases. What no one saw coming was all three happening at the same time.

On top of monetary tightening, the government failed to reach its target of 400,000 jobs in December. They only managed to add 199,000 new jobs. Though this did have a major effect on the unemployment rate, it is certainly not a positive sign heading into the new year.

It is also important to understand how the new variant, Omicron, will impact FED’s raising interest rates. If there is a delay, we can see risk-on assets like bitcoin go in the other direction. But suppose they reduce their balance sheet aggressively and hike interest rates with less time gap. In that case, it will be extremely difficult to navigate through any kind of financial market, especially crypto.

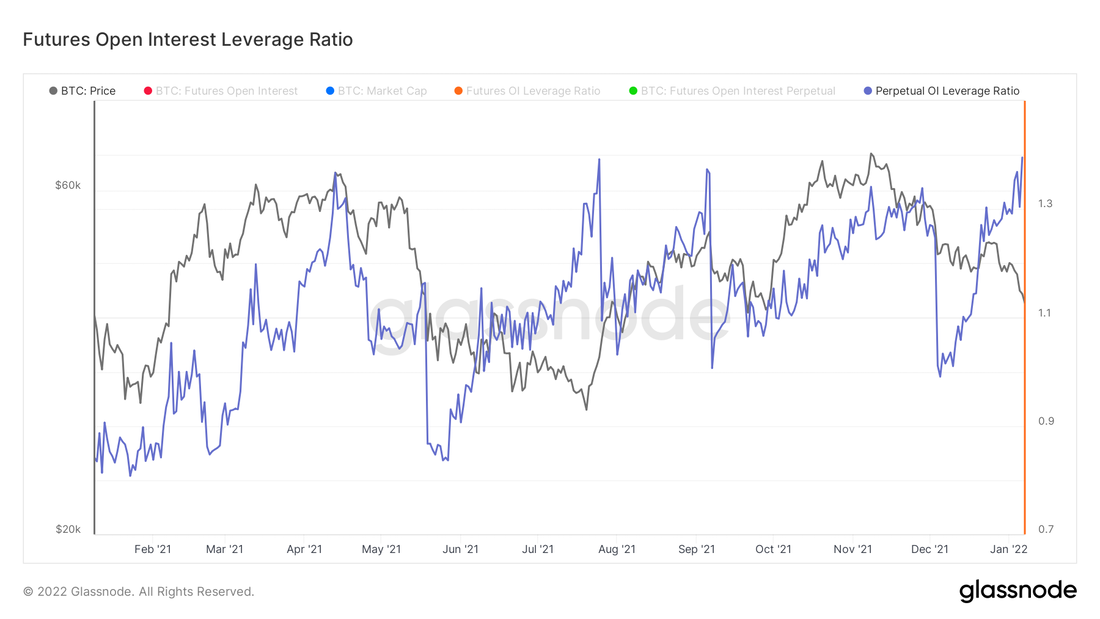

With bitcoin, we need to pay attention to the perpetual futures market in crypto. We can see extreme volatility is coming, and pressure is building up in the leveraged markets. But we don’t know the positioning of market participants. To overcome this risk management challenge with bitcoin, we need to look at funding rates. We wanted to see mixed and negative funding rates for the last couple of months. But it was pretty much a flat line. So there was no indication of a short squeeze setup, like the one we saw in late July 2021.

So, even though we saw major liquidation events over the past few weeks, we cannot conclude that the market is not any longer going to make any violent moves, at least in the short term. The stablecoin market interest is still near its ATH, so we have a long way to go to see a complete flush out in the futures market. I emphasize the equities side of markets because bitcoin is a risk on/off the asset. As it is now institutionalized, there is a high correlation with other financial markets.

In terms of on-chain metrics, we can look at the following and understand the overall market sentiment.

Global In/Out of the Money

When bitcoin went on a tear and hit a new ATH at $69k, the majority of the market thought it was inevitable that BTC would reach 100k by the end of 2021. So we saw a lot of buying in those high 60 levels. As a result, more than 34% of the active addresses are in a state of impermanent loss. If we reclaim the $53k level, we will quickly see these losses turn into p

Supply Held by Long-Term Holders

The famous on-chain analyst, Checkmate, creates the chart below. This is an important metric to understand long-term holders’ spending and buying behavior. They are the ones that established the floor for bitcoin. So if there is anything fundamentally going wrong, we can use this metric for validation. Currently, we are not seeing any major spike in supply held by LTH. In Q4 2021, we saw BTC distribution for a short period, reducing the total supply held by LTH by 1.11%. This has also flatlined. So the main takeaway here is long-term holders are not selling at these prices and are slowly accumulating.

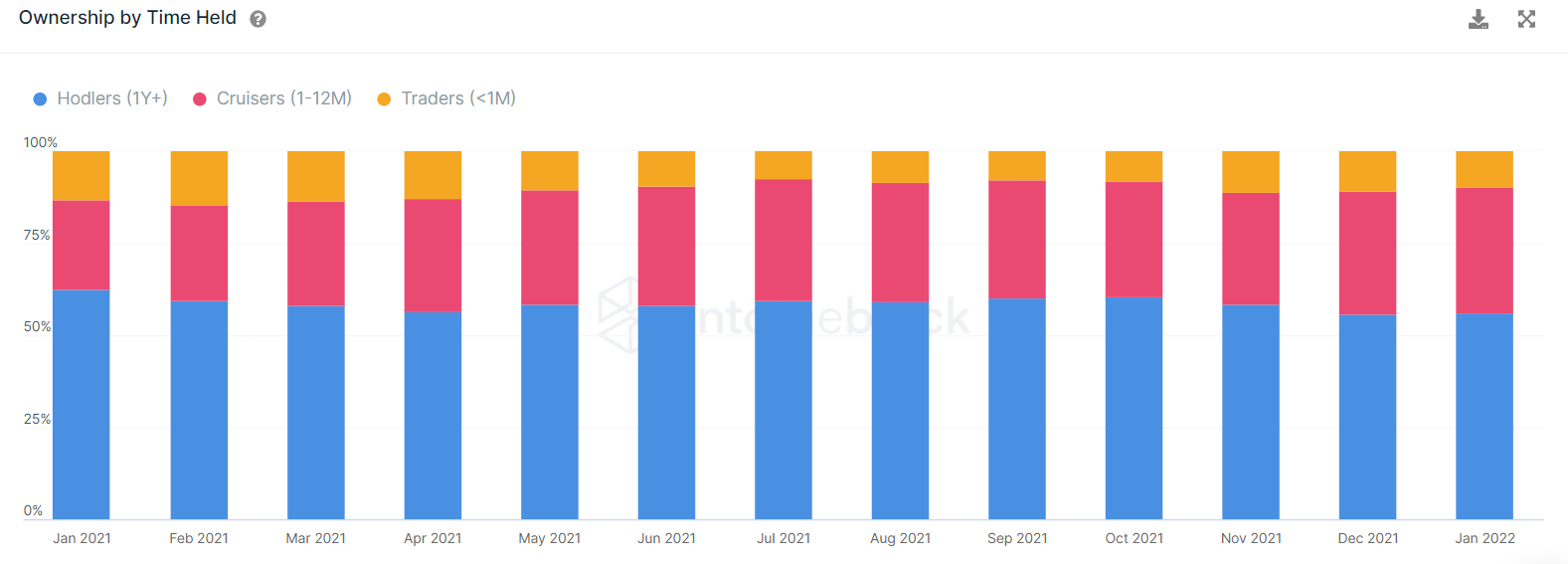

Ownership by Time Held

Over the past year, so many cruisers and traders turned into holders, strengthening the concentration of ownership of BTC. At the moment, we are seeing more than 50% of BTC addresses as holders and less than 10% as traders. It is also important to note that the number of traders over the last two months has been down drastically, which means most of the market is not looking for any bitcoin traders in this choppy market.

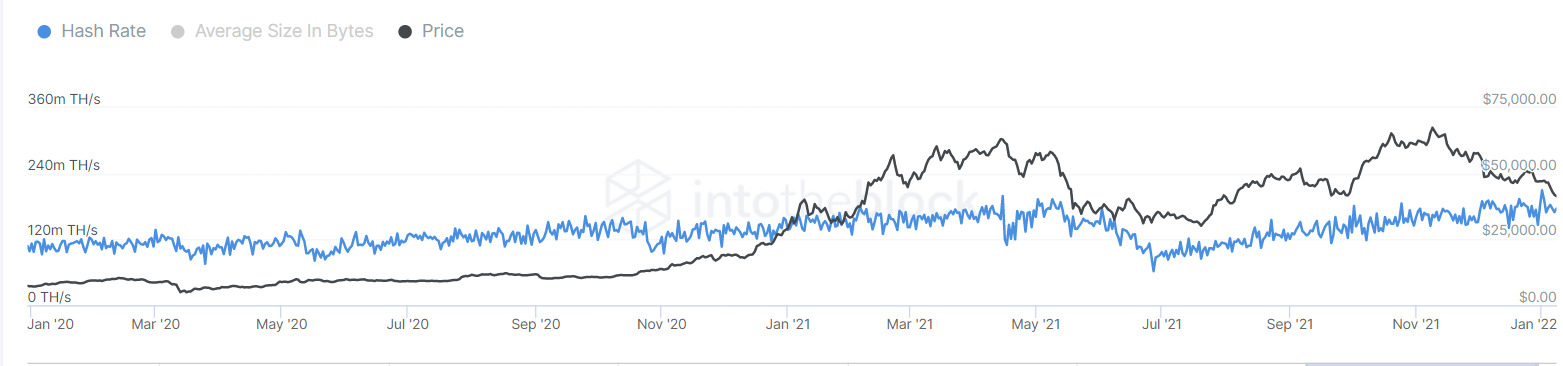

Hash Rate

I am throwing in this chart because of the recent shutdown of mining activities in Kazakhstan. As it is one of the top mining spots, we need to see any major impact on the bitcoin network. We saw a little dip to low 160m TH/s. But nothing serious. This is a very good sign, considering we saw a complete crash in June 2021. We made a perfect recovery and hit an all-time high of 210m TH/s.

Final Thoughts

Bull Case

We assumed this would be an extended bull cycle when we had the first major liquidation and failed to reach our $100k target. If that’s still our thesis, we need to see BTC reclaim $53k in the next few weeks. That alone wouldn’t be enough. We need to see mainstream participation from institutions and public companies to add BTC, showing a high-level conviction towards this asset class. This will likely change the market sentiment and help initiate a strong rally.

Bear Case

There is no single metric or data point showing us we are beginning a new bear cycle. The on-chain network stats are showing overall positive signs. But from a general market perspective, we are seeing many things go wrong. The price action is broken and fundamentals are starting to change. So the public sentiment is shifting bearish quickly. After the FED hearing, it got worse. Considering this is a new year, it is not a good start for crypto in any way. For comparison, the same happened in 2017 with altcoins. Many of them did huge rallies, acting as exit liquidity. In this cycle, we assume it is going to be NFTs.

What I am trying to say is — do not continue with this mindset of “diamond hand forever” and ignore how the overall market structure is looking. With NFTs pumping hard, it could easily be liquidity for whales to exit. So plan your exit strategy accordingly.

Born and brought up in India, Karthikeya Gutta is a crypto journalist and freelance contributor for ItsBlockchain. He covers various aspects of the industry with in-depth analysis and research. His passion towards blockchain and crypto ecosystem is mainly because he believes it can really change the world and help millions of people.

Subscribe to get notified on latest posts.

{kind=link}